MEASURING FINANCIAL LITERACY:

CONCEPTUAL STUDY

CONCEPTUAL STUDY

Sudindra

V R

V R

1. INTRODUCTION:

Unlike

traditional roles played by governments and employers in managing investments

on behalf of individual significantly transformed in recent past due to change

in social structure across the world. It

is responsibility of individuals in managing their own finance to secure their

financial future. In the complex

financial environment, it is imperative that individuals develop nuanced

understanding of world of finance to meet their financial goals and needs. It

is observed that most of the individuals under-saved, fail to invest wisely and

continued to be overburdened with loans/advances.

traditional roles played by governments and employers in managing investments

on behalf of individual significantly transformed in recent past due to change

in social structure across the world. It

is responsibility of individuals in managing their own finance to secure their

financial future. In the complex

financial environment, it is imperative that individuals develop nuanced

understanding of world of finance to meet their financial goals and needs. It

is observed that most of the individuals under-saved, fail to invest wisely and

continued to be overburdened with loans/advances.

2.

CONCEPT

OF FINANCIAL LITERACY:

CONCEPT

OF FINANCIAL LITERACY:

OECD-

Organization of Economic Co-operation and Development, defines financial

literacy is a combination of awareness, knowledge, skills , attitude and

behaviors necessary to make sound financial decisions and ultimately achieve

individual financial wellbeing.

Organization of Economic Co-operation and Development, defines financial

literacy is a combination of awareness, knowledge, skills , attitude and

behaviors necessary to make sound financial decisions and ultimately achieve

individual financial wellbeing.

3.

COMPONENTS

OF MEASURING FINANCIAL LITERACY:

COMPONENTS

OF MEASURING FINANCIAL LITERACY:

Measuring

financial literacy requires a clear understanding of financial literacy

concepts and application of appropriate evaluation tools.

financial literacy requires a clear understanding of financial literacy

concepts and application of appropriate evaluation tools.

Major components of financial

literacy includes:

literacy includes:

Ø Savings/borrowings: basic understanding of savings alternatives, different

types of savings account, borrowing procedures, debt literacy and ability to

plan for future.

types of savings account, borrowing procedures, debt literacy and ability to

plan for future.

Ø Personal budgeting:

understanding of personal budgeting, budget balance, taxation impact on income,

disposable income and estimation using appropriate measures.

understanding of personal budgeting, budget balance, taxation impact on income,

disposable income and estimation using appropriate measures.

Ø Economic issues:

understanding of economic situation, economic ratio’s, knowledge of economic

terms and etc.

understanding of economic situation, economic ratio’s, knowledge of economic

terms and etc.

Ø Financial concepts:

understanding of time value of money, risk and returns, risk profiling, timing

in investments and other related concepts.

understanding of time value of money, risk and returns, risk profiling, timing

in investments and other related concepts.

Ø Financial services:

knowledge of financial products, services, mechanism of card services,

insurance, broking services, online services and other financial services.

knowledge of financial products, services, mechanism of card services,

insurance, broking services, online services and other financial services.

Ø Investing:

understanding of investment opportunities, risk and rewards and other investment

related risks.

understanding of investment opportunities, risk and rewards and other investment

related risks.

4.

OECD

FINANCIAL LITERACY MEASUREMENT DEVELOPMENT PROCESS:

OECD

FINANCIAL LITERACY MEASUREMENT DEVELOPMENT PROCESS:

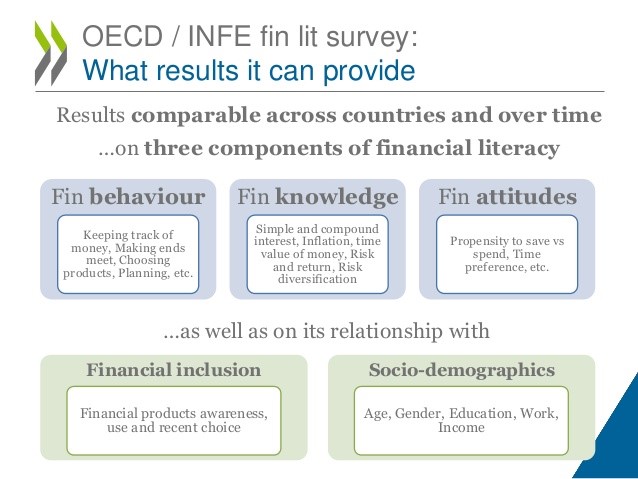

Based

on 18 existing survey from 16 countries, OECD developed international good

practice in financial literacy measurement. With support and guidance from expert sub

group developed survey instrument (questionnaire), which covers attitude and

knowledge as well as capturing behavior related topics like money management,

planning, financial/investment goals and awareness of financial product &

financial services.

on 18 existing survey from 16 countries, OECD developed international good

practice in financial literacy measurement. With support and guidance from expert sub

group developed survey instrument (questionnaire), which covers attitude and

knowledge as well as capturing behavior related topics like money management,

planning, financial/investment goals and awareness of financial product &

financial services.

Measurement

instrument must achieves the following objectives:

instrument must achieves the following objectives:

Ø Questionnaire

must be based on widely accepted definition of financial literacy which

emphasis general behavior, attitude and knowledge.

must be based on widely accepted definition of financial literacy which

emphasis general behavior, attitude and knowledge.

Ø All

the components of financial literacy must be able to identify the relationship

with financial product awareness, use and recent choices and socio demographic:

age, gender, education, work and income variables.

the components of financial literacy must be able to identify the relationship

with financial product awareness, use and recent choices and socio demographic:

age, gender, education, work and income variables.

Ø It

should be read loud by an interviewer and consists of Likert type scales.

should be read loud by an interviewer and consists of Likert type scales.

Ø It

should be market specific questions: such as product awareness, access to

information about the product and comparable to international data.

should be market specific questions: such as product awareness, access to

information about the product and comparable to international data.

Ø It should stress on individual capacity to

draw on savings is relative rather than absolute. Focused on amount of time

they could manage for, rather than the amount of money they have saved.

draw on savings is relative rather than absolute. Focused on amount of time

they could manage for, rather than the amount of money they have saved.

Ø Sequential

approach to review product awareness to ensure respondents not made to feel

financially excluded.

approach to review product awareness to ensure respondents not made to feel

financially excluded.

5.

CONCLUSION:

CONCLUSION:

Traditionally

government use to play vital role in managing investment of individuals but in

today’s complex environment, individuals has to manage their own finance their

future financial goals and needs. It is observed that most of individuals are

under-saved, fail to invest wisely and indebtedness. To understand level of

financial literacy majorly savings/borrowing, personal budge, economic issue,

financial concepts, financial service, financial product and investment

components can be consider. OECD developed the instrument based on existing

survey which considered widely accepted definition, market specific questions,

focused rather than absolute and sequential review of product awareness.

government use to play vital role in managing investment of individuals but in

today’s complex environment, individuals has to manage their own finance their

future financial goals and needs. It is observed that most of individuals are

under-saved, fail to invest wisely and indebtedness. To understand level of

financial literacy majorly savings/borrowing, personal budge, economic issue,

financial concepts, financial service, financial product and investment

components can be consider. OECD developed the instrument based on existing

survey which considered widely accepted definition, market specific questions,

focused rather than absolute and sequential review of product awareness.

<https://www.oecd.org/finance/financial-education/49319977.pdf>