Investor Psychology

& Market Rationality Argument

& Market Rationality Argument

KIRAN KUMAR K V

Market Rationality

Argument

Argument

There

are certain suppositions upon which markets work. It assumes that human beings are rational, in fact, always rational. Their sole objective

is to maximize the return for a given level of risk that they are taking. The

concept of risk-adjusted return, that’s the foundation block of many asset

pricing and valuation models, highlights the risk-aversion behaviour of investors. Risk-aversion relates to the

behaviour of individuals under uncertainty. If an individual is offered two

options: one, where he will get Rs. 50 for sure and two, a gamble with a 50%

chance of getting Rs. 100 and another 50% chance of getting nothing. The

investor may react in three ways: He may choose the latter and gamble; He may

choose the former and be conservative; He may choose to be indifferent, as the

expected value before the bet in both the cases is Rs. 50

are certain suppositions upon which markets work. It assumes that human beings are rational, in fact, always rational. Their sole objective

is to maximize the return for a given level of risk that they are taking. The

concept of risk-adjusted return, that’s the foundation block of many asset

pricing and valuation models, highlights the risk-aversion behaviour of investors. Risk-aversion relates to the

behaviour of individuals under uncertainty. If an individual is offered two

options: one, where he will get Rs. 50 for sure and two, a gamble with a 50%

chance of getting Rs. 100 and another 50% chance of getting nothing. The

investor may react in three ways: He may choose the latter and gamble; He may

choose the former and be conservative; He may choose to be indifferent, as the

expected value before the bet in both the cases is Rs. 50

When

he chooses to gamble, he is referred to as risk-seeker. A risk-seeking or

risk-loving investor chooses uncertainty over certainty, as he gets extra ‘utility’ from the uncertainty associated

with the gamble. It can be observed in individual’s behaviors like buying a

lottery, or gambling in a casino or even sitting on a giant wheel. Risk-seekers

are also the ones who calculate the risk. Let’s consider in the above example,

if the latter option gave a 40% chance of getting Rs. 50 and 60% of nothing, a

risk-seeker may have avoided the gamble.

he chooses to gamble, he is referred to as risk-seeker. A risk-seeking or

risk-loving investor chooses uncertainty over certainty, as he gets extra ‘utility’ from the uncertainty associated

with the gamble. It can be observed in individual’s behaviors like buying a

lottery, or gambling in a casino or even sitting on a giant wheel. Risk-seekers

are also the ones who calculate the risk. Let’s consider in the above example,

if the latter option gave a 40% chance of getting Rs. 50 and 60% of nothing, a

risk-seeker may have avoided the gamble.

When

he chooses to be indifferent, the investor is referred to as risk-neutral.

He is an investor who cares only about the return. Uncertainty is not at all a

parameter of analysis for a risk-neutral investor. A risk-neutral behaviour can

be found when the investment at stake is insignificant part of their wealth.

he chooses to be indifferent, the investor is referred to as risk-neutral.

He is an investor who cares only about the return. Uncertainty is not at all a

parameter of analysis for a risk-neutral investor. A risk-neutral behaviour can

be found when the investment at stake is insignificant part of their wealth.

If an investor chooses the

guaranteed income over gamble, he can be referred to as a risk-averse investor. He

will generally shy away from risky investments, even if the return is lower as

long as it is guaranteed. That does not mean he will not at all take risk. It

just means that he is not comfortable with the return he is getting for the

amount of risk he is assuming. He looks for a risk-return tradeoff that results

in that extra-utility for him. Because individuals are different in their

preferences, all risk-averse individuals may not rank investment alternatives

in the same manner. Take the example of Rs. 50 gamble; all risk-averse

individuals will rank the guaranteed outcome of Rs. 50 higher the option of

gambling the same. What would have happened if the guaranteed outcome was Rs.

40 and not Rs. 50? Some risk-averse investors might consider Rs. 40 inadequate,

others might accept it, and still others might become indifferent. This

suggests that individuals are risk-averse and they prefer more to less. They

are also able to rank different investment alternatives in order of their

preference and such ranking are internally consistent. Such utility function is

represented by the economist’s function:

guaranteed income over gamble, he can be referred to as a risk-averse investor. He

will generally shy away from risky investments, even if the return is lower as

long as it is guaranteed. That does not mean he will not at all take risk. It

just means that he is not comfortable with the return he is getting for the

amount of risk he is assuming. He looks for a risk-return tradeoff that results

in that extra-utility for him. Because individuals are different in their

preferences, all risk-averse individuals may not rank investment alternatives

in the same manner. Take the example of Rs. 50 gamble; all risk-averse

individuals will rank the guaranteed outcome of Rs. 50 higher the option of

gambling the same. What would have happened if the guaranteed outcome was Rs.

40 and not Rs. 50? Some risk-averse investors might consider Rs. 40 inadequate,

others might accept it, and still others might become indifferent. This

suggests that individuals are risk-averse and they prefer more to less. They

are also able to rank different investment alternatives in order of their

preference and such ranking are internally consistent. Such utility function is

represented by the economist’s function:

Where,

U is the utility function, E(r) is the expected return and

is the variance of the investment and A is the measure of risk-aversion. It

can be computed as the marginal reward that an investor requires to accept a

unit of additional risk. A higher risk-averse investor requires greater

compensation for accepting additional risk (a higher A) and vice versa.

U is the utility function, E(r) is the expected return and

is the variance of the investment and A is the measure of risk-aversion. It

can be computed as the marginal reward that an investor requires to accept a

unit of additional risk. A higher risk-averse investor requires greater

compensation for accepting additional risk (a higher A) and vice versa.

Apparent Irrationality

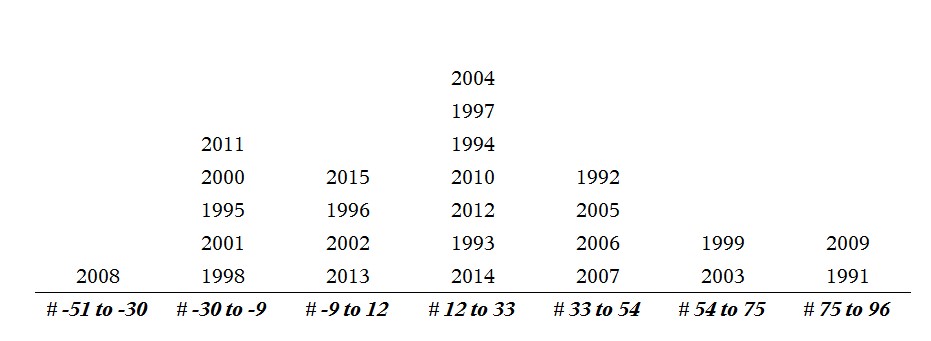

Below presented is the data of

the number of years when BSE Sensex has given a specific range of return

intervals. For example, two years, viz., 1991 and 2009 were the years when the

annual returns of Sensex were in the range of 75% to 96%.

the number of years when BSE Sensex has given a specific range of return

intervals. For example, two years, viz., 1991 and 2009 were the years when the

annual returns of Sensex were in the range of 75% to 96%.

Figure 1: Sensex Returns 1991-2015 (Source: Author’s Calculation) |

The

non-normal distributions of returns of Indian stocks in the past 25 years or so

show that there is a positive skewness. That also means there is higher

frequency of positive deviations from the mean. If the investors were rational

and always took the right decisions in terms of computing their risk-adjusted

returns, the distribution of returns must have been normal (assuming the

central limit theorem could be applied here, as Sensex in itself a portfolio of

30 companies and we are attempting to present returns for 25 years). The only

conclusion we can draw is that there is an anomaly here that is either

underestimating or overestimating the risk (as measured by the standard

deviation) by the investing community.

non-normal distributions of returns of Indian stocks in the past 25 years or so

show that there is a positive skewness. That also means there is higher

frequency of positive deviations from the mean. If the investors were rational

and always took the right decisions in terms of computing their risk-adjusted

returns, the distribution of returns must have been normal (assuming the

central limit theorem could be applied here, as Sensex in itself a portfolio of

30 companies and we are attempting to present returns for 25 years). The only

conclusion we can draw is that there is an anomaly here that is either

underestimating or overestimating the risk (as measured by the standard

deviation) by the investing community.

Investor Psychology as an Explanation

While the major blocks of investment finance,

like the mean-variance portfolio, CAPM, investor rationality and risk-return

trade-off have been the ingredients in valuation and security analysis models

widely used in real world, there is also an argumentative perspective to the

(above-discussed) basic tenet upon which such models are constructed.

Behavioural Finance questions the very assumption that people are guided by

reason and logic and independent judgment. It is also possible that investors

are not rational, at least always, and emotions and herd instincts might be

playing a role in influencing their investment decisions. This approach attempts to enumerate

explanations why individuals make the decisions they do, irrespective of

rationality. Few such behavioural inconsistencies are discussed below to give

an idea of the approach:

like the mean-variance portfolio, CAPM, investor rationality and risk-return

trade-off have been the ingredients in valuation and security analysis models

widely used in real world, there is also an argumentative perspective to the

(above-discussed) basic tenet upon which such models are constructed.

Behavioural Finance questions the very assumption that people are guided by

reason and logic and independent judgment. It is also possible that investors

are not rational, at least always, and emotions and herd instincts might be

playing a role in influencing their investment decisions. This approach attempts to enumerate

explanations why individuals make the decisions they do, irrespective of

rationality. Few such behavioural inconsistencies are discussed below to give

an idea of the approach:

–

Representativeness

Bias: A tendency to form judgments based on stereotypes. An

investor may see the effect of a policy rate change by the central bank based

on historical trend

Representativeness

Bias: A tendency to form judgments based on stereotypes. An

investor may see the effect of a policy rate change by the central bank based

on historical trend

–

Anchoring

Bias: A tendency to be unwilling to change an earlier

decision, despite a new, relevant information arrival

Anchoring

Bias: A tendency to be unwilling to change an earlier

decision, despite a new, relevant information arrival

–

Familiarity

Bias: A tendency to be comfortable with things that are

familiar to them. Being familiar with employer or the industry they work in

people tend to invest in the known sectors.

Familiarity

Bias: A tendency to be comfortable with things that are

familiar to them. Being familiar with employer or the industry they work in

people tend to invest in the known sectors.

–

Affect

Heuristic Bias: A tendency to go by the gut feel or intuition.

Affect

Heuristic Bias: A tendency to go by the gut feel or intuition.

–

Innumeracy

Bias: A tendency to give more focus on big numbers and less

weight to small figures. Ignoring the base rate, wrongly counting the

probability of an event

Innumeracy

Bias: A tendency to give more focus on big numbers and less

weight to small figures. Ignoring the base rate, wrongly counting the

probability of an event

–

Loss

Aversion Bias: A tendency of people to dislike losses more than they

like comparable gains. Many overreactions or panic selling in market we have

witnessed occur due to this bias. Especially, in countries like India, where

generally the retail investors are largely conservative in their risk appetite,

we see an increased overreaction

Loss

Aversion Bias: A tendency of people to dislike losses more than they

like comparable gains. Many overreactions or panic selling in market we have

witnessed occur due to this bias. Especially, in countries like India, where

generally the retail investors are largely conservative in their risk appetite,

we see an increased overreaction

–

Narrow

framing Bias: A tendency of investors to focus on

issues/events/portfolios in isolation and respond based on hos such issues are

posed

Narrow

framing Bias: A tendency of investors to focus on

issues/events/portfolios in isolation and respond based on hos such issues are

posed

–

Mental

Accounting Bias: A tendency of investors to keep track of gains and

losses for different investments in separate mental accounts and treat those

accounts differently

Mental

Accounting Bias: A tendency of investors to keep track of gains and

losses for different investments in separate mental accounts and treat those

accounts differently

–

Shadow

of the Past Bias: A tendency of people to consider a past outcome as a

factor in evaluating a current risky decision. A Snake-bite effect refers to the behaviour where individuals being

less inclined to take risk after a incurring a loss.

Shadow

of the Past Bias: A tendency of people to consider a past outcome as a

factor in evaluating a current risky decision. A Snake-bite effect refers to the behaviour where individuals being

less inclined to take risk after a incurring a loss.

–

Herd

Instinct Bias: A tendency to move with the group, even if one has a contradicting

solution

Herd

Instinct Bias: A tendency to move with the group, even if one has a contradicting

solution

The

biases discussed above are just a few examples of what behavioural finance

approach assumes to be the reasons for markets being inefficient (i.e., market

prices always uncorrelated with any known variable). Behavioural finance thus

can be seen as a contrasting approach to the traditional investment finance

theory and the market efficiency theory. Behavioural finance seems to have

answers for irrationality of market prices in converging with the intrinsic

value.

biases discussed above are just a few examples of what behavioural finance

approach assumes to be the reasons for markets being inefficient (i.e., market

prices always uncorrelated with any known variable). Behavioural finance thus

can be seen as a contrasting approach to the traditional investment finance

theory and the market efficiency theory. Behavioural finance seems to have

answers for irrationality of market prices in converging with the intrinsic

value.

Behavioural biases affect all

market participants. Now the question is how do rebuild the asset pricing or

valuation models to account for behavioural biases such that all the factors –

rational & irrational (behavioral) – that influence the price discovery in

security markets are accounted for and fully reflect the causations of given

market behaviour. If there can be a model that can do this, market participants

would be able to recognize, respond and make improved decisions, individually

and collectively.

market participants. Now the question is how do rebuild the asset pricing or

valuation models to account for behavioural biases such that all the factors –

rational & irrational (behavioral) – that influence the price discovery in

security markets are accounted for and fully reflect the causations of given

market behaviour. If there can be a model that can do this, market participants

would be able to recognize, respond and make improved decisions, individually

and collectively.

References: Behaviour Finance, Chandra, 2016; Investopedia; IAPM, Reilly & Brown, 2014